You probably already know I struggle with oversharing on this blog once in a while. That’s why I’ve written about that time I noticed my toenails were less than they should be. I’ve also written about how I struggle with gratitude, which shouldn’t be the case, but for whatever reason, is. Perhaps the gratitude is overshadowed. Nothing more, nothing less. It’s there, but it’s clouded. That’s how I feel today on the heels of what was undoubtedly another remarkable year for me. I ended the year with more than $130,000,000 in closed transactions, which positioned me as the number one agent in Walworth County for the seventh year in a row. Without the trust of my customers and clients, I wouldn’t be here today, and I know that every potential client in this market could easily choose anyone but me. So for that, I remain indebted to you, and I promise to do everything I can to guide you through this challenging market. But I digress, there are more meaningful things afoot. Notably, a surprise issue of Summer Homes For City People: The Winter Issue.

In the new magazine, I combine the typical nonsensical stories about whatever is on my mind, along with some great imagery of homes I’ve sold and have for sale, and in the case of the 2023 Winter Issue; lots of data. Data, after all, is what makes the real estate world function. Or is it? Is it data, or is it simply client pursuit and client capture, combined with commissions? I might argue that’s what really makes the world of real estate tick, but alas, there is lots of data heading your way, packaged in a glossy issue that I do hope you like. You can look for that around Lake Geneva sometime in the next two weeks.

In the new issue, I write a few bits about where I see the market moving in 2023. To save you from painful anticipation, here’s a piece from the new issue…

If there’s one lesson to learn from 2022 it’s that inventory, or the pronounced absence of it, overrides all obvious market headwinds. If interest rates are up, equity returns are down, crypto is in free-fall, and covid era geographic displacements have slowed, then it should make good sense to see a high flying vacation home market in decline. And if not in decline, then certainly on pause. The issue is with a slow drip of inventory and a steady supply of buyers, a market cannot find itself in decline. Let’s pretend we began 2022, with those high equity indices and those rock bottom interest rates, with 150 active lakefront buyers across all valuation segments. Now let’s assume that after the second quarter, wherein we saw interest rates double and equity valuations decline by 20%, we lost 30% of those buyers. That means we now only have 105 buyers seeking to purchase inventory in a market that would only see a dozen or so transactions all year. If you were wondering why Lake Geneva has held up so well through this cycle, it’s all about the inventory.

Looking forward, what would we need to see prices suffer any meaningful decline? For the sake of the conversation, let’s assume 10% of the current valuations are pure fluff, and that for a decline to be measurable and moderately painful it would need to exceed 15%. What would force prices to drop by such a percentage? The answer is inventory. And not only inventory, but a return to more historical inventory totals. It’s hard to imagine today, but Lake Geneva would typically offer between 25 and 40 on market lakefront properties at any given point in time. For the majority of 2021 and 2022, we had fewer than 10 open market listings, and for many periods, including during this winter season, we had just one lakefront available property. If we need inventory to rise for prices to decrease, can you imagine just how much unsold inventory we would need to add to see that happen?

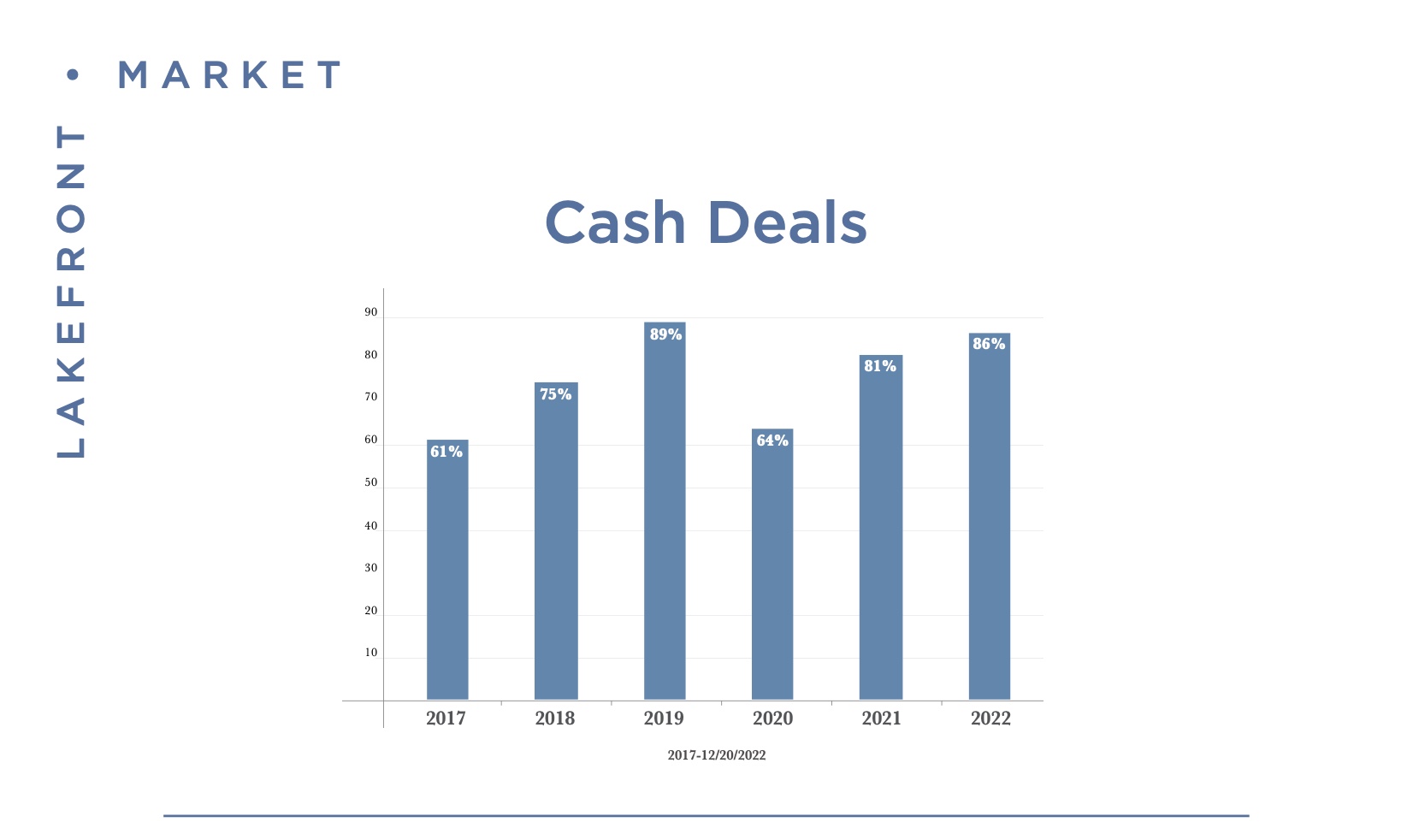

If a seller was concerned about the future softening of the market, they would have sold when interest rates doubled and equities dropped. What would the new catalyst be to send inventory back to historical levels? For one, a continued and painful decline in equity markets. SPY $400 doesn’t leave anyone fearful, in the same way that SPY $300 might. Along those lines, interest rates have had little impact on our markets (see the chart for cash transactions in our recent transaction history), but interest rates that continue to climb into the 8% range might very well shake a few sellers loose (if they have any adjustable debt on their balance sheet). Beyond that, I believe it would take a catastrophic event during 2023 to push inventory to the levels that it would create a meaningful decline in valuations. Absent that catastrophe, I expect 2023 to look quite similar to 2022, with lighter volume and stiff valuations. The nuance in the market means that sellers still need to price their properties with proper respects paid to market trends and comparable data. Even with our limited inventory during 2022, there were sellers who were forced to adjust their overshot target valuations in order to attract buyers. For buyers, it means valuations will be difficult for the coming year, but that doesn’t mean that value will be impossible to discover. Buyers should be seeking blue chip properties, and should seek proper counsel to understand which properties are worthy of their premiums and with ones are not. That’s why I’m here, to quiet the noise of this market and help you make sense of it all.